Should a problem for everyone be solved by the few?

December 2nd, 2015

December 2nd, 2015

At last month’s G20 Leaders’ Summit in Antalya, Turkey, leaders of some of the world’s largest economies endorsed measures to plug loopholes in international taxation that allow transnational corporations to dodge taxes. But as drafting of the initiative, known as the Base Erosion and Profit Shifting (BEPS) recommendations, has come to a close, the focus now turns to implementation. G20 Leaders called on the OECD to develop an inclusive framework for implementation that includes developing countries on ‘equal footing’.

However, after excluding non-G20 developing countries from decision making through the agenda setting and design process, calling for their involvement on ‘equal footing’ at the implementation stage may appear patronising rather than inclusive. If there is anything we can learn from the BEPS process, it is that being a member of institutions that are tasked with finding a global solution matters.

The political mandate for the OECD BEPS project came from the G20, so G20 leaders and Finance Ministers are ultimately the ones to hold accountable for the flawed process they have endorsed. Many have highlighted the technical gaps in the BEPS measures, but the process itself is worrying. The 3 essential stages were:

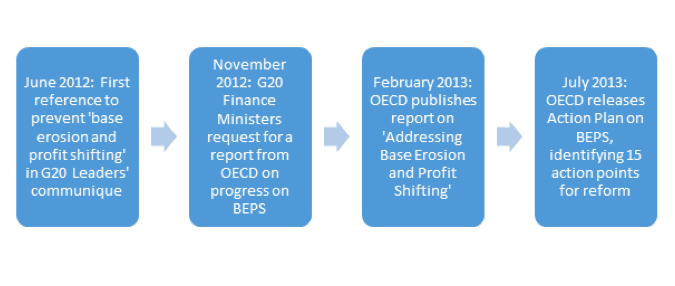

Timeline of the agenda setting process

After the G20 recognised base erosion and profit shifting to be a global problem, it is unclear why they mandated the OECD to lead the project. The OECD has been honest about the fact that the agenda setting process didn’t involve developing countries, as indeed it’s not within their mission. Quoting from their website,

“The BEPS Action Plan was drafted over a very short period of time as the public concern and the political pressure rose significantly at the end of 2012. Because of this time pressure, the diagnosis of the root causes of BEPS (BEPS Report, February 2013), the development of the BEPS Action Plan (BEPS Action Plan) and the adoption of this plan (G20 declaration) mainly involved the OECD/G20 countries.”

It is important to put this sense of urgency in perspective. Developing countries have long complained about the need for reform of the international tax standards and rules. This was conveniently ignored until OECD countries realised they were victims of their own inadequate rules. The public outrage, most notably in the EU, where citizens faced austerity measures while corporations were dodging taxes, is what finally led G20/OECD to move to address the issue.

Meanwhile, the G77 (group of 134 developing countries) has repeatedly recognised the UN Tax Committee as a more inclusive tax body that has more legitimacy than the OECD. Rather than increasingly relying on the OECD to serve as the G20’s unofficial think tank on global tax matters, it would have been prudent of the G20 to instead invest in the UN tax committee to lead this process from the outset.

Not surprisingly, the OECD came under near immediate criticism for the lack of involvement of developing countries and the organisation acknowledges that they moved to correct that after the BEPS Action Plan was adopted.

“…directly after the BEPS Action Plan was adopted, broad consultations took place with developing countries, using all the mechanisms feasible (questionnaires distributed through many channels, including channels of the United Nations (UN) and the World Bank Group (WBG); Global Forum meetings attracting more 300 delegates from over 100 countries and international and regional organisations; joint events with the UN; 5 regional consultations; the Tax and Development program; the Global Relations programme).”

Already late in the process, the consultations were not set up to succeed. At the BEPS regional consultations, developing countries raised the issue that the balance between source and residence taxation is significant for them, but were told by OECD that is beyond the scope of the BEPS agenda. This issue of allocation of taxing rights raised by developing countries is fundamental to a flawed international tax system that favours countries where corporations are headquartered (mostly OECD and G20 countries) as opposed to ‘source countries’ or developing countries. It is no surprise then that an OECD reform agenda privileges rich country priorities as the most immediate. This is a prime example cited by G77 leaders in their demands for an intergovernmental UN tax body that will reflect a broader set of global priorities.

In response to criticisms, the OECD then launched another consultation process or what they referred to as a ‘new structured dialogue process’ in November 2014, more than a year after first launching its BEPS Action Plan. This dialogue was intended around three pillars:

“1) the direct participation of developing countries and of Regional Tax Organisations in the Committee on Fiscal Affairs of the OECD and all technical working groups; (2) the set-up of Regional Networks of tax policy and administration officials on BEPS in five regions to ensure the participation of countries that are not able to regularly attend the Paris-based meetings; (3) capacity building support, including the development of toolkits, to assist countries implement solutions to tackle BEPS.”

It’s important to note here that direct participation in the Committee on Fiscal Affairs meant that select developing countries (Albania, Azerbaijan, Bangladesh, Croatia, Georgia, Jamaica, Kenya, Morocco, Nigeria, Peru, Philippines, Senegal, Tunisia, and Vietnam) and regional organisations such as African Tax Administrators Forum (ATAF) were invited to attend meetings and able to ‘provide input at the working and decision-making levels’ [emphasis added]. The subtext is that some non-G20 developing countries are welcome to provide input, but will still not be on equal footing with OECD/G20 countries in decision making, what OECD refers to as ensuring “an efficient process.”

After endorsing an exclusive plan which ensured that non-G20/OECD countries didn’t get to participate on equal footing, there are now calls to get all countries involved in implementation on an equal footing. In addition, the plan now offers “capacity building.” In international dialogues on tax matters, capacity building while needed in some contexts is unfortunately used more often to deflect attention from the structural issue being raised.

The policy exchange typically goes like this:

Developing Countries: The international system of allocating taxing rights designed in the 1920s by rich countries do not work for us. There needs to be more political dialogue on balance of source and residence taxation.

OECD governments: That is not a priority for us since our countries benefit from this system. But we will design a reform agenda that is a priority for us and then build your capacity to implement those measures instead.

Developing Countries: We want a seat at the table to design global tax rules that benefit all countries. Developing countries are hardest hit by tax dodging and UN is the only inclusive institution that can address this.

OECD governments: Here, take Addis Tax Initiative, Tax Inspectors without Borders, and more capacity building instead! Can everyone stop whining about this already?

This is not to suggest that capacity building is unimportant. But offering capacity building in response to repeated calls to address systemic issues with distorted global standards is utterly beside the point. It might also be appropriate for OECD countries to think twice: given recent scandals around Apple, Google, Amazon, and Starbucks not paying taxes in OECD countries themselves, what capacity is there to transfer? If there is, they may want to keep it at home and start using it.

Some have argued that there is no real need for a global tax body, since developing countries can work through regional bodies or unilaterally to bring in reforms. Okay, then let’s be consistent. Both OECD and UN should stop setting tax standards that are global. If having different regional and national standards is truly a better way forward, this would put the OECD out of the global standards business too. This is somewhat tongue-in-cheek, since of course multinationals would still be looking for global solutions to ease their ability to work across countries. But at least it would be fair.

Setting aside this thought experiment, let’s say we can’t get past the need for global cooperation and some standard setting on tax. Then we must also not pretend that there are no consequences to which institution leads those efforts. The UN tax committee is currently an obscure technical committee with members acting in personal capacity and the committee is devoid of any real resources. But it’s also the only forum addressing the critical issue of source-based taxation that’s so important to most of the world’s population. Why not empower it?

Developing countries are not asking the OECD to stop doing work that represents the OECD’s interests. The G77 are merely arguing for political backing and resources for the only forum that represents their interests by upgrading it to an intergovernmental body with core UN funds. Ensuring there is no duplication across institutions is a discussion worth having. But as long as OECD countries continue to be obstinate blockers on the UN body, it’s impossible to have a meaningful conversation.

China and India as G20 and BRICS hosts in 2016 have a responsibility to prioritise their UN tax body ask

BRICS – the group of 5 rapidly growing economies: Brazil, Russia, India, China and South-Africa – have been central to pushing for international tax reforms and challenging OECD tax standards. India and Brazil particularly, showed leadership in the Financing for Development (FfD) negotiations in backing G77’s call for an intergovernmental UN tax body, a proposal blocked successfully by OECD countries. Yet, their endorsement in G20 of a flawed process has been disappointing to watch.

BRICS leaders bear the responsibility to push the inclusive tax body forward in political negotiations simply because they have nothing to lose in the process. They can afford to move unilaterally on tax reforms if required and reject capacity building that may not be in their best interest. BRICS economies are generally not dependent on aid. This may be less true for other developing countries who might choose to be vocal on this issue.

With China as next year’s G20 host and India hosting the BRICS Summit in 2016, there’s a real opportunity next year for the BRICS nations to walk the talk on representing developing countries’ interests in the G20. 134 developing countries have long demanded the UN Tax Committee to be upgraded to an inclusive, intergovernmental body with core UN funds. China and India are well-positioned to demonstrate their leadership and take this agenda forward in influential global forums they are part of in 2016.