Where should we make the rules? A look at how the UN can help tackle IFFs

May 19th, 2017

May 19th, 2017

Just shy of two years since the 3rd Financing for Development Conference was held in Addis Ababa, governments, civil society and policymakers will come together again. But rather than set new ambitions, we’ll be following up on the commitments of the past.

The Financing for Development Follow-Up Forum takes place at the United Nations headquarters from 22-25 May and the aim is to see how we’re doing in regards to financing development, including mobilizing domestic resources. With curbing illicit financial flows so key to unlocking desperately needed resources, it’s an apt time to take stock of what governments have committed to so far, and what remains to be done.

The inclusion of a target in the Sustainable Development Goals on reducing illicit financial flows (target 16.4), is an important recognition by countries globally on the development implications of illicit financial flows. There is much to be done by countries at the national and regional level, but for a global problem involving cross-border movement of illicit money, ignoring what needs to be achieved through international cooperation is no longer an option. As leaks such as Panama Papers, Swiss Leaks and Lux Leaks only seem to happen with more frequency, the extent of global financial secrecy is becoming more and more apparent.

The first Financing for Development (FfD) Conference, the Monterrey Consensus in 2002, acknowledged the need to address ‘capital flight’. But it was the second FfD Conference, the Doha Declaration in 2008, where member states noted that it was ‘vital to address the problem of illicit financial flows’. Then, at the third FfD Conference, the Addis Ababa Action Agenda reiterated the issue with a commitment to ‘redouble efforts’ to reduce illicit financial flows. Criticism of the emptiness of the rhetoric of such commitments will be difficult for governments to counter, if we don’t see effective political actions at this stage.

Two issues in particular are politically significant:

The FfD conferences, particularly the Addis Ababa Action Agenda (AAAA), failed to deliver on concrete ‘actions’ that would signal to citizens that governments are serious about cooperating on illicit financial flows. Member states committed to ‘scale up’ international cooperation and ‘enhance disclosure practices and transparency’ in both source and destination countries — crucial steps towards reducing illicit financial flows enabled by financial secrecy. Yet, they only endorsed existing initiatives of limited ambition rather than ramping up their efforts. They endorsed country-by-country reporting by multinational corporations to tax authorities instead of ensuring this was published to enable investors, parliamentarians, journalists, academics and civil society to have a more informed conversation on impacts of tax planning strategies of corporations. There was no commitment to establish public registers of beneficial owners, or the natural persons who ultimately control or profit from a company or other legal entities, a critical transparency reform to deter the use of anonymous shell companies aiding crime and corruption. Crucially, one of the most ambitious proposals during the negotiations — an institutional mechanism to ensure inclusive intergovernmental cooperation on these issues through a UN intergovernmental tax body — was blocked by US, UK, EU, Japan and other developed countries who argued that OECD is the appropriate forum for such cooperation.

Similar disagreement continued in the UNCTAD negotiations in 2016. The UNCTAD outcome document ‘Maafikiano’ is divided into two sections: problem analysis and mandate. The mandate section is what allows UNCTAD — an important UN institution unique in its ability to work at the intersection of trade, finance and development – to decide the scope of their work. Yet, there is only an acknowledgement of the need to address illicit financial flows in the ‘problem analysis’ section but developed countries once again blocked another UN institution from being mandated to carry out any meaningful work on it.

Member States have also agreed in the UN that addressing illicit financial flows has important human rights and gender implications. The 61st Session of the ECOSOC Commission on the Status of Women (CSW) in 2017 noted the importance of combatting illicit financial flows to ensure resource gaps are closed for achieving gender equality. UN Independent Human Rights Experts have noted that mechanisms that allow wealthy individuals and corporations to evade or avoid taxes through complex transactions across multiple tax havens means that governments end up relying on more regressive sources of revenue, the burden of which falls the hardest on the poor, especially women. It also undermines efforts to build effective institutions to uphold civil and political rights.

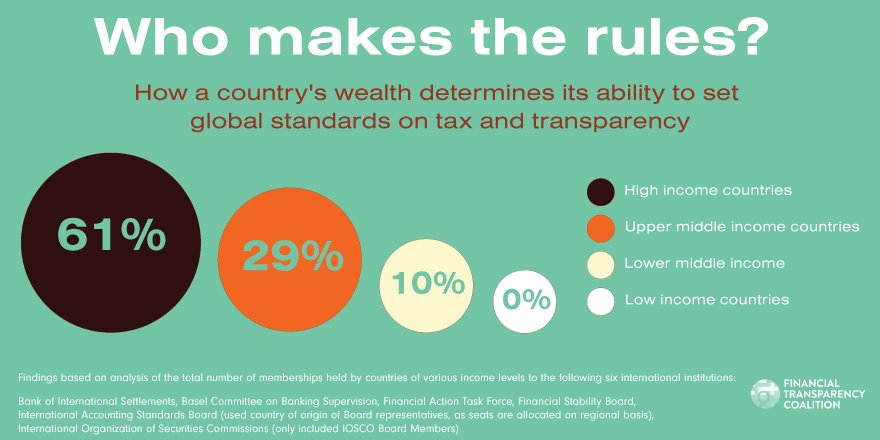

To summarise, all countries have committed to the UN addressing illicit financial flows but don’t agree on empowering UN institutions to actually follow through on delivering this ambitious commitment. It perhaps isn’t surprising to note the pattern of developed countries blocking the UN from being the inclusive space for setting international standards on these issues — membership of current institutions leading on making rules in relation to IFFs is largely limited to wealthy nations. From OECD to Financial Action Task Force (FATF) to G20 — most developing countries are excluded in designing the agenda and standards on issues related to IFFs.

Noting this imbalance in representation, G77 and China (group of 134 developing countries) have repeatedly pushed for an intergovernmental body at the UN to address issues in relation to illicit financial flows, including tax evasion and avoidance.

The other issue where there is no intergovernmental consensus is the conceptual framework for illicit financial flows, particularly whether tax avoidance should be included. G77 and China has been in favour of a wider definition, noting their ‘concern over illicit financial flows and related tax avoidance and evasion, corruption and money-laundering by using certain practices, with negative impacts for the world economy, in particular for developing countries’ (emphasis added). On the other hand, some of the OECD countries have favoured focusing more strictly on illegal aspects such as corruption, crime, tax evasion and money laundering. This working paper by the FfD Office provides a helpful overview of the various definitions and positions.

– There is as yet no global architecture for tackling IFFs. There are a number of commendable initiatives and instruments to deal with .. IFFs, but they are often disparate

– The processes are not universal and at times are undertaken by various countries and groups in their own interests with no obvious interface between them

– It might be important to consider how best all these elements could fit into an overarching global framework, perhaps under the auspices of the United Nations

Report of the High Level Panel on Illicit Financial Flows from Africa, UNECA (page 73)

The Report of the High Level Panel on Illicit Financial Flows from Africa defines IFFs as “money illegally earned, transferred or used” but clarifies that this includes tax avoidance noting that “The various means by which IFFs take place in Africa include abusive transfer pricing, trade mispricing, misinvoicing of services and intangibles and using unequal contracts, all for purposes of tax evasion, aggressive tax avoidance and illegal export of foreign exchange”

It’s past time for the rhetoric around illicit financial flows in the UN to translate to meaningful action, but this requires governments to reach an agreement on two unresolved political issues — establishing a universal, intergovernmental tax body at the UN for inclusive international cooperation on these issues and agreeing on a robust framework for defining illicit financial flows. Otherwise, as one commentator noted wryly, member states will commit at the next FfD Conference to perhaps ‘retriple’ efforts (having ‘redoubled’ efforts at Addis Ababa) to reduce illicit financial flows.