Developing countries’ access to CbCR: Guess who’s (not) coming to OECD dinner

May 5th, 2017

May 5th, 2017

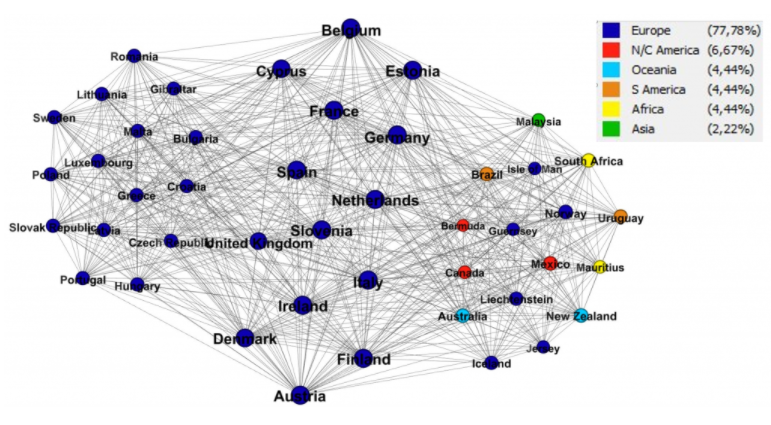

The OECD has just made available the list of activated relationships to automatically exchange country-by-country reports between countries. They use big figures like 700 relationships, but don’t get fooled by those numbers – simply look at the image below to see who really has access to CbCR.

Oh, by the way, there’s nothing wrong with your eye-sight. Developing countries are just not there.

Source: Rasmus Christensen (https://twitter.com/phdskat/status/860093952992608256?s=09), by kind permission

The problem is that instead of requiring a fully multilateral approach, the OECD has allowed bilateral relationships to the automatic exchange of CbCR. This makes it harder for more jurisdictions to exchange CbCR, and more costly to arrange – and in practice results in the exclusion of nearly all lower-income countries:

Some jurisdictions also continue to work towards agreeing bilateral competent authority agreements for the automatic exchange of CbC Reports with specific partners under Double Tax Conventions or Tax Information Exchange Agreements

Now, think of a major country that doesn’t appear on the image and is definitely choosing the bilateral approach when it comes to non-OECD countries. Hint 1: its very many multinationals (MNEs) have aggressively pursued profit shifting, so that the misalignment of their global profits away from the locations of their real economic activity has gone from just 5% in the 1990s to more than 25% now. Hint 2: this country won’t be joining the CRS (the global framework for automatic exchange of banking information) either.

Yes indeed: it’s our old friend, Tax Haven USA.

Treas rep: US will not be exchg’g CbC reports w countries where we don’t have treaty or TIEA & they can’t ask for this info under OECD agt

— MindyHerzfeld (@InternationlTax) May 3, 2017

But the number of current activated relationships is not a problem of developing countries only. Out of the close to 200 jurisdictions where MNEs are likely to have operations, so far only 53 jurisdictions have chosen the multilateral approach (instead of the bilateral one) and thus signed the Multilateral Competent Authority Agreement (MCAA) to exchange the CbCR with each other.

Out of those 53 signatories, so far only 30 jurisdictions have indicated with which other jurisdictions they want to exchange the CbCR in practice– just like the framework for automatic exchange of banking information, the MCAA for CbCR also has a dating system, where jurisdictions may cherry-pick with whom to have an agreement to exchange CbCR in practice (a “qualifying agreement” in the words of the OECD).

Out of the 30 jurisdictions that already chose their “CbCR-dating partners”, one would expect that they will all exchange the CbCR with each other (so all would have qualifying agreements with each other). Not surprisingly, this is not the case. So far, Brazil will only exchange CbCR with other 27 jurisdictions, Malaysia and Uruguay with 26, Mexico with 25 and Bermuda, a main part of the famous Double-Irish Dutch Sandwich scheme to avoid taxes, will only exchange CbCR with 23 jurisdictions.

If you are not confused enough about the process, it gets even trickier. Countries may also choose whether to require filing of the CbCR by the MNE’s headquarters, to allow voluntary filings by headquarters during a transition period, or to allow for a surrogate to file the CbCR. This is a “clear” explanation published now by the OECD:

While the Action 13 report recommends that jurisdictions provide up to 12 months after the end of the reporting fiscal period for filing of the CbC report, jurisdictions may apply an earlier filing deadline. Currently, around 45 jurisdictions have implemented an obligation for the filing of CbC Reports by resident UPEs. An MNE group may also nominate a constituent entity to act as a surrogate parent entity (SPE) and file a CbC Report on a voluntary basis. In this case, the SPE may also be the UPE of an MNE group (e.g. this may be done where the jurisdiction of the UPE does not require the filing of CbC Reports for a particular reporting fiscal period, but has its legislation in place and allows filing on a voluntary basis) or it may be a constituent entity in a different jurisdiction that allows filing of CbC Reports by SPEs. Currently 10 countries have informed the OECD that they will permit voluntary parent surrogate filing by the resident UPE of an MNE group, and around 45 countries will permit surrogate filing by constituent entities that are not the UPE of their group.

(If you want the complicated version, look at the OECD Model legislation here.)

On the bright side, the complex framework to access CbCR (explained by TJN here in detail and here graphically) does not depend on countries signing the MCAA or even having a qualifying agreement (being chosen back in the dating system). A country would still be allowed to obtain the CbCR automatically from a second “surrogate” country (instead of receiving the CbCR from the country where the MNE’s are headquartered), or even better, eventually require the CbCR from any local subsidiary of an MNE (local filing).

On the down side, however (and this very down indeed), the whole process, from automatic exchanges to local filings, depends on countries having an international agreement[1] in place not with any other country, but with the country where the MNE is headquartered[2] (even if they will end up receiving the CbCR from a surrogate country or from a local subsidiary, they still need to have the international agreement with the headquarters’ jurisdiction).

Opposite to this nonsense process, public CbCRs, easily accessible to all of the world’s tax authorities and to journalists and civil society, is the obvious ideal solution – CbCRs could simply be published by each MNE’s on their website. But the OECD rejected this. The second best, good only for the world’s tax authorities (not for civil society and journalists), is to have all MNE’s subsidiaries “locally filing” the CbCR with their local tax authority (after all, once the CbCR has been produced, the same 2-page document should be accessible to all relevant tax authorities). But again, the OECD rejected this, making local filing available only under extraordinary circumstances, and threatening to penalize countries that try to access the CbCR beyond OECD’s restrictions.

Vietnam, caring more about fighting tax avoidance than to obey OECD’s arbitrary restrictions, decided to require local filing, whenever it cannot obtain the CbCR automatically from other countries. If countries want to ensure access the CbCR they should do the same.

Tax prof Yariv Brauner agrees, talking about the obstructive US position:

An empty threat. Nonexchangable countries can simply demand it in audit or by domestic legislation. Not playing by the rules goes both ways. https://t.co/xiTPfkZqh2

— Yariv Brauner (@YarivBrauner) May 4, 2017

The OECD, in the meantime, will try to prevent this, ostensibly. Only look at how much it abhors local filing (we highlighted the OECD explanation in bold for an easier read):

A summary here:

In order to (…) and avoid local filing wherever possible, the OECD is working with jurisdictions to..

The full explanation here (our emphasis):

While not forming part of the Action 13 minimum standard, in exceptional circumstances a jurisdiction may require the filing of a CbC Report by a resident constituent entity that is not the UPE of its group (referred to as local filing). There is no requirement for a jurisdiction to apply local filing, but where it does so this may be applied only in three specific circumstances.

Even where one of these conditions is met, local filing is not permitted where a CbC Report will be filed by an SPE of the MNE group for the relevant reporting fiscal period (subject to conditions) or where the residence jurisdiction of the constituent entity does not meet conditions in the minimum standard concerning consistency, confidentiality and the appropriate use of CbC Reports.

In order to provide certainty to groups which need to prepare for the filing of CbC Reports by UPEs or SPEs, and avoid local filing wherever possible, the OECD is working with jurisdictions to support them in putting in place as early as possible an obligation on resident UPEs to file a CbC Report and qualifying competent authority agreements with other jurisdictions with which they plan to exchange CbC Reports.

It’s true that not playing by the rules goes both ways. But it’s also true that it’s much easier for a global power to resist the club of which it is the biggest member, than for lower-income countries that don’t even have a seat at the table.

One last point to note: looking back at @phdskat’s great figure (included again below for ease) on who is agreeing CbCR exchange, the dark blue dominates completely. In other words, current OECD tax cooperation is basically the EU, plus a few. Assuming the US continues an obstructionist-cum-withdrawal stance on this important element of multilateralism, one of two things can happen. Either the OECD becomes a more progressive, less conflicted body able to move somewhat more quickly on issues the US has blocked – like public CbCR – and with the ‘Inclusive Forum’ allowing lower-income countries to exert some genuine control over the organisation’s direction; or the centre of power on international tax issues shifts from the OECD to the EU. Neither outcome is necessarily great for global governance, compared to the emergence of a leading UN body on tax. But the former has some attraction, and both could give rise to greater progress than otherwise during the Trump administration.

Source: Rasmus Christensen (https://twitter.com/phdskat/status/860093952992608256?s=09), by kind permission

[1] For example, a double tax agreement (DTA), a tax information exchange agreement (TIEA) or being a party to the Amended Multilateral Tax Convention, as long as the country where the MNE is headquartered is also party to the amended Multilateral Tax Convention.

[2] An international agreement is not necessary if the country where the MNE is headquartered does not require the MNE to file the CbCR, or if, after exchanging information automatically, it fails to keep doing it.