A Setback in Fighting Tax Avoidance in India: Vodafone vs. Union of India

March 9th, 2012

March 9th, 2012

In a judgment having far-reaching consequence, a three judges bench of the Supreme Court of India, in the case of Vodafone International Holdings BV v. Union of India, has set aside the Mumbai High Court judgment, which had required Vodafone to pay capital gains tax worth US$2.5 billion to the Government of India for a transaction that had seen the company acquire 67 per cent stake in Hutchison Essar (a mobile phone operator in India) in 2007. Vodafone, the second largest telecom operator in India, had challenged the tax bill over its US$11.5 billion deal to buy Hutchison Whampoa Ltd.’s Indian mobile business in 2007, and appealed to the Supreme Court (SC) after losing the case in the Mumbai High Court.

Vodafone’s main argument was that the Government of India cannot levy taxes because the transaction was made between non-Indian companies outside the country; the deal was between Vodafone International Holdings BV – a Dutch subsidiary of Vodafone – and CGP Investments Ltd., a Cayman Islands company, which held the Indian telecom assets of Hutchison. Indian tax authorities, however, held that the transaction was taxable because the assets acquired by Vodafone are based in India.

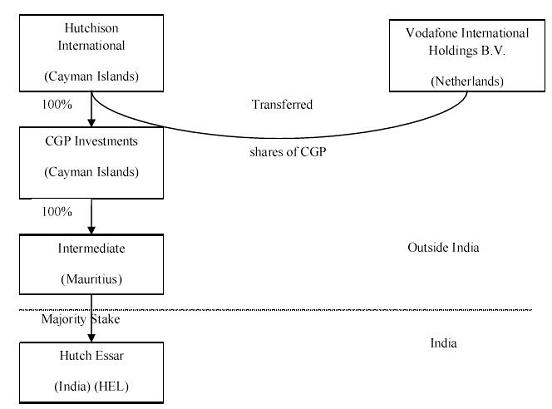

The below diagram taken from here illustrates how this transaction was structured, enabling the transfer of shares of an Indian company to take place outside India.

Tax Guru

Prashant Bhushan, a Supreme Court lawyer in India, notes that the use of holding companies and subsidiaries (as highlighted in the above diagram) for tax avoidance is a lucrative industry in the world that flourishes with the help of big accountancy and consultancy firms in the name of ‘tax planning’.

Finally, the Supreme Court ruled in favor of Vodafone and directed the Indian Income Tax department to return 25 billion rupees (approx $475 million) deposited by Vodafone, in compliance of its interim order, within two months along with 4 percent interest.

Implications

With a combined gross fiscal deficit of central and states placed at 8.1% of GDP in 2011-12 by the Reserve Bank of India, the loss of much-needed revenue to the government is important to note. But beyond the immediate loss of revenue, the fallout of the ruling is larger as a number of multinationals operating in various sectors such as SABMiller (brewery), Sanofi Aventis (pharmaceuticals), Kraft Food, and Vedanta (extractive industries) have entered into acquisition deals similar to that of Vodafone. Sandeep Ladda, executive director with PricewaterhouseCooper (PwC) India, said,

“This settles a prolonged litigation that had created a lot of uncertainty for foreign companies having similar structures who had entered into or were proposing to enter into similar transactions”

The impact of the ruling on FDI has been much debated. Unsurprisingly, India Inc. and various chambers have lauded the SC ruling for upholding the law which will send positive signals to foreign investors and be beneficial for foreign direct investment (FDI) in the long run. As per Secretary General of FICCI (Federation of Indian Chambers of Commerce and Industry) Rajiv Kumar,

“Stability of institutional processes is an important requirement for attracting foreign direct investment. This decision will re-inject confidence in cross-border mergers and acquisitions and further augment such investment coming to India”.

But this judgment has also been criticized for legitimizing the use of artificial devices for tax avoidance in the name of ‘tax planning’ that the Court should allow and encourage to attract foreign direct investment.

Tax Justice Network notes that if the SC had ruled in favor of Indian tax authorities, while the corporations may have grumbled about the investment climate, they would still be scrambling to invest in the Indian telecommunications market knowing that it is a goldmine.

Government of India also recently moved the SC seeking review of the judgment noting that it was surprised by the apex court’s decision to give relief to Vodafone on the ground that its offshore transaction was a structured foreign direct investment (FDI) into the country when in reality not a single rupee came as investment into India. In its 101-page review petition, the Ministry of Finance through its Secretary and the Assistant Director of Income-tax has noted that the FDI policy was in no way under challenge or scrutiny in the instant case and could not have been so as the FDI and interpretation of taxing statutes operate in two different realms.

While the debate now focuses on what changes will be made to the tax laws to address such cases in the future (including introducing GAAR), perhaps it is pertinent to note a previous Supreme Court ruling in the judgment of McDowell and Co. in 1985 which observed that,

“It is neither fair nor desirable to expect the legislature to intervene and take care of every device and scheme to avoid taxation. It is up to the Court to take stock to determine the nature of the new and sophisticated legal devices to avoid tax and … to expose the devices for what they really are and to refuse to give Judicial benediction”

{kind=link}