UNEQUAL

EXCHANGE

How poor countries are blindfolded in the

global fight against banking secrecy

RECEIVING INFORMATION IS HALF THE BATTLE

While it's helpful for jurisdictions to receive information, almost just as important is where the information is coming from. For example, if Kenya is receiving information from Mali, that's great, but what might be more beneficial for recouping lost tax revenue is to receive information from places like Mauritius, Switzerland, or the Cayman Islands, places that are known to harbor offshore assets.

The below interactive allows you to search through our data analysis to see the specific relationships a jurisdiction has, where it sends information, and from where it receives information.

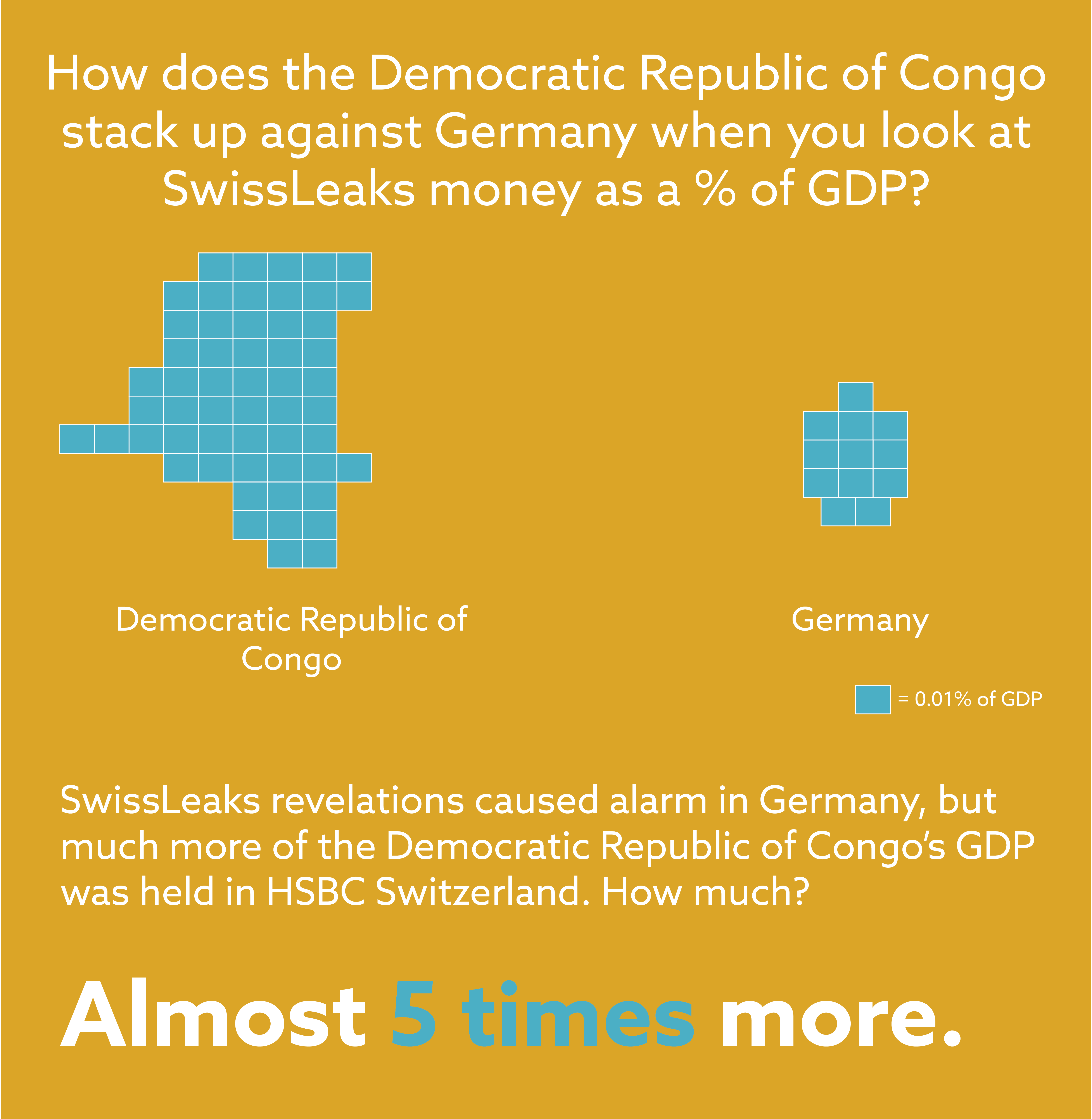

FIGHTING TAX ABUSE WITH A BLINDFOLD ON

Receiving financial account information is vital for governments around the globe, but perhaps no more so than in the Global South, where tax revenues, both in total amounts and also as a percentage of GDP, are far lower than in the north. Increased resources are desperately needed to fund key drivers of development, such as roads, schools and health infrastructure.

As we revealed in a 2015 project called SwissLeaks Reviewed, poor countries are disproportionately exposed to the risks of the offshore system. While the absolute amounts of money leaving their borders may be smaller, when viewed as a proportion of the country’s Gross Domestic Product, the amounts often surpass those found in wealthy nations.

For example, the Democratic Republic of Congo had nearly five times more offshore wealth connected to the Swiss Leaks scandal than Germany, when considered as a percentage of GDP. Similarly, the exposure of Central African Republic was eleven times that of the USA and the figure for Kenya nine times that of Canada. The list goes on.

And this is not a theoretical concern. With the information made available through Swiss Leaks, in 2015 Spain claimed it recovered roughly $340 million in taxes and fines. When applying a similar rate of return to the money connected to Sierra Leone, for example, the potential revenue could be about $4.95 million*. Though $5 million may sound paltry at the onset, the fact that the potential tax revenue from just one bank in just one secrecy jurisdiction could equate to roughly 19% of the country's health budget is simply shocking.

But tax authorities should not have to rely on occasional leaks for such information. Without access to the world's information exchange systems, many low and even middle-income countries will be fighting cross-border tax evasion with a blindfold on.

The below interactive allows you to search our data based on a jurisdiction's income level. Countries that do not appear are not currently receiving information via the automatic exchange agreements analyzed.

*Spain/Sierra Leone figures calculated in Sept 2015, using exchange rates of that time.

This is a joint project of Christian Aid and the Financial Transparency Coalition. Reach out to us about the project here.

Special thanks to Code for Africa, a Pan-African civic technology lab that designed our data visualizations.

Click here to download our raw data, or here for a two-page explainer on the data.